However, many tax systems permit all assets of a similar type acquired in the same year to be combined in a “pool”. Depreciation is then computed for all assets in the pool as a single calculation. These calculations must make assumptions about the date of acquisition. One half of a full period’s depreciation is allowed in the acquisition period (and also in the final depreciation period if the life of the assets is a whole number of years). United States rules require a mid-quarter convention for per property if more than 40% of the acquisitions for the year are in the final quarter.

What if the useful life of an asset is short?

The depreciation expense can be projected by building a PP&E roll-forward schedule based on the company’s existing PP&E and incremental PP&E purchases. For the same example, what will be the depreciating expense if the company charges 20% per annum? If you use a vehicle or piece of equipment exclusively for business, you can claim depreciation on that asset. However, if you drive a car for work and for personal use, you can only claim depreciation on the business portion of your tax return (for example 60% of the cost). The company sets a percentage amount for depreciation costs rather than the useful life years of an asset. In our example above, the company can decide to allocate a 15% depreciation cost.

The amount an asset is depreciated in a given period of time is a representation of how much of that asset’s value has been used up. These accounting rules stipulate that physical, tangible assets are to be depreciated and intangible assets are amortized, although there are schedule of accounts payable exceptions for non-depreciable assets. The credit side of the amortization entry may go directly to the intangible asset account depending on the asset and materiality. Depreciation entries always post to accumulated depreciation, a contra account that reduces the carrying value of capital assets. In this method, the depreciated percentage is charged on the net book value of a fixed asset.

This netbook value is the remaining balance of fixed asset cost after deducting the overall depreciation charged for the previous years. Thus, the depreciable value diminishes every year, and so does the depreciated expense. The value of the assets gets depleted due to constant use for business purposes. Companies depreciate to account for this value throughout the useful life of that asset. It is a fixed cost for the companies, and the amount depreciated can be used to purchase new machinery after the old one turns into a scrap.

The Modified Accelerated Cost Recovery System, or MACRS, is another method for calculating accelerated depreciation. This works well for vehicles, equipment, and other physical assets, but it cannot be used for intangible assets. The General Depreciation System (GDS) is the most common method for calculating MACRS. In accounting, depreciation is recorded as an expense that gradually reduces the book value of an asset. Since an asset benefits your business over an extended period, this expense is recorded over time to allocate the asset’s cost over the periods it benefited the company. Sum-of-years-digits is a spent depreciation method that results in a more accelerated write-off than the straight-line method, and typically also more accelerated than the declining balance method.

- The concept of useful life represents the period beyond which it would not be practical to use an asset anymore.

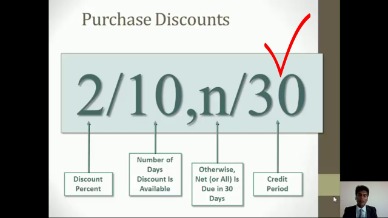

- Tax depreciation is different from depreciation for managerial purposes.

- New assets are typically more valuable than older ones for a number of reasons.

- In some cases, an asset may decline in value at a steady rate, while others may decline more rapidly in years where they see heavier use.

- The depreciation expense is scheduled over the number of years corresponding to the useful life of the respective fixed asset (PP&E).

Create a Free Account and Ask Any Financial Question

The salvage value represents the cost the company expects to recover at the end of the machine’s useful life. After deducting this residual value from the fixed asset cost, the value acquired is divided by the useful life of the fixed assets. MACRS calculations tend to be a more complicated method for calculating depreciation and may benefit from the support of a tax professional. Since double-declining-balance depreciation does not always depreciate an asset fully by its end of life, some methods also compute a straight-line depreciation each year, and apply the greater of the two.

The notes may contain the payment history but a company must only record its current level of debt, not the historical value less a contra asset. strong letter for outstanding payment templates Almost all intangible assets are amortized over their useful life using the straight-line method. Depreciation is recorded to reflect that an asset is no longer worth the previous carrying cost reflected on the financial statements. Both methods appear very similar but they’re philosophically different.

Double declining balance depreciation

The double declining balance method is often used for equipment when the units of production method is not used. Machinery and equipment are expensive assets for a company to purchase. This allows the company to match depreciation expenses to related revenues in the same reporting period—and write off an asset’s value over a period of time for tax purposes. Wear and tear is the most common cause of depreciation for a fixed asset. Any asset gradually breaks what is variable costing down over time as parts wear out and need to be replaced.

A business might buy or build an office building and use it for many years. The original office building may be a bit rundown but it still has value. The cost of the building minus its resale value is spread out over the predicted life of the building with a portion of the cost being expensed in each accounting year. For a complete depreciation waterfall schedule to be put together, more data from the company would be required to track the PP&E currently in use and the remaining useful life of each. Additionally, management plans for future capex spending and the approximate useful life assumptions for each new purchase are necessary.

The key difference between amortization and depreciation involves the type of asset being expensed. There are also differences in the methods allowed, including acceleration. Components of the calculations and how they’re presented on financial statements also vary. The straight-line depreciation method gradually reduces the carrying balance of the fixed asset over its useful life. Depreciation is the decline in the book value of a fixed asset over time. When you have a fixed asset like a vehicle, building, or piece of equipment, these things will naturally suffer some wear and tear over time.